Our January blog article, Zero Can Be Your Hero: Why Flat Doesn’t Mean Failure in IUL Design, focused on why a 0% floor is a mathematical safety net when designing IUL policies. February’s deep dive takes that logic into the next phase of planning: resilience through distribution. It is easy to illustrate high returns in a vacuum, but real financial wellness is built on how a policy performs under imperfect conditions. In this sequel to last month’s analysis, we are stress-testing a new case example using a 200-basis-point haircut to the AG49 rate dropping it from 6.59 to 4.59% and a forced 0% index credit every fifth year.

For this case, we modeled a 49-year-old male (Standard Non-Tobacco) in Connecticut. To ensure the strategy was built for maximum efficiency and minimum drag, we utilized the following design parameters:

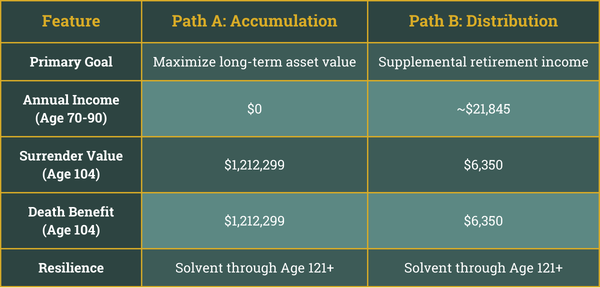

We then ran this single funding pattern through two distinct paths: one focused purely on long-term accumulation and the other on controlled income/distributions.

This design solves for a minimum face amount and allows the cash value and death benefit to grow without the impact of loans or withdrawals.

Even with the haircut and periodic 0% years, the policy remains a powerhouse. By age 104, surrender values reach over $1.2 million while maintaining a level $240,000 death benefit. In this scenario, the internal rate of return (IRR) on surrender value settles in the mid-3% range by life expectancy—proving that a well-designed policy can deliver robust value even under significant market pressure.

The second ledger demonstrates how the same $240,000 total outlay can be pivoted to support a retirement income strategy.

Starting around age 70, we illustrated annual distributions via fixed loans running through approximately age 90. Despite the stressed credits, the design supports an annual income stream of approximately $21,845 for 21 years. The policy not only stays in force but preserves a meaningful residual death benefit, with IRRs remaining in the same 3%+ range over the full horizon.

It is important to remember that, at its core, an IUL is a life insurance contract, and like any permanent structure, there are internal costs associated with the death benefit protection. These mortality and expense charges are the trade-off for the security the policy provides.

However, this scenario highlights why design is the ultimate equalizer. By intentionally overfunding the policy—pairing a minimum death benefit with the maximum allowable premium—we direct as much capital as possible toward the cash value. This strategy ensures that even in flat years or under haircut crediting rates, the growth from the premium itself can outpace the pure insurance charges, preventing the policy from stagnating.

Outcomes will always vary, and no one can predict future index performance. But when an IUL is designed with realistic expectations—minimum face for efficiency and disciplined funding—the chassis works. Whether your client needs a long-term tax-advantaged asset or a source of supplemental income, a conservative design ensures that the improbable stays probable.

Do you have a perplexing case requiring expert advanced design? Reach out to us at OnTheCase@ThreePointsInsuranceDesign.com today.