IUL debates are nothing new, but with the Kyle Busch/Pacific Life IUL lawsuit making headlines, the product’s mechanics are getting even more attention than usual. While high-profile litigation often focuses on performance expectations, there is a persistent myth that if the index posts 0%, the IUL will lose cash value.

In reality, many IULs credit 0% instead of a negative return, ensuring that losses from the index do not directly hit the cash value. When the design uses a minimum non-MEC death benefit and maximum allowable premium, more of each dollar goes to cash value instead of pure insurance charges, which helps the value grow even through flat years.

To put this to the test, we modeled a worst-case scenario that would make most skeptics blink.

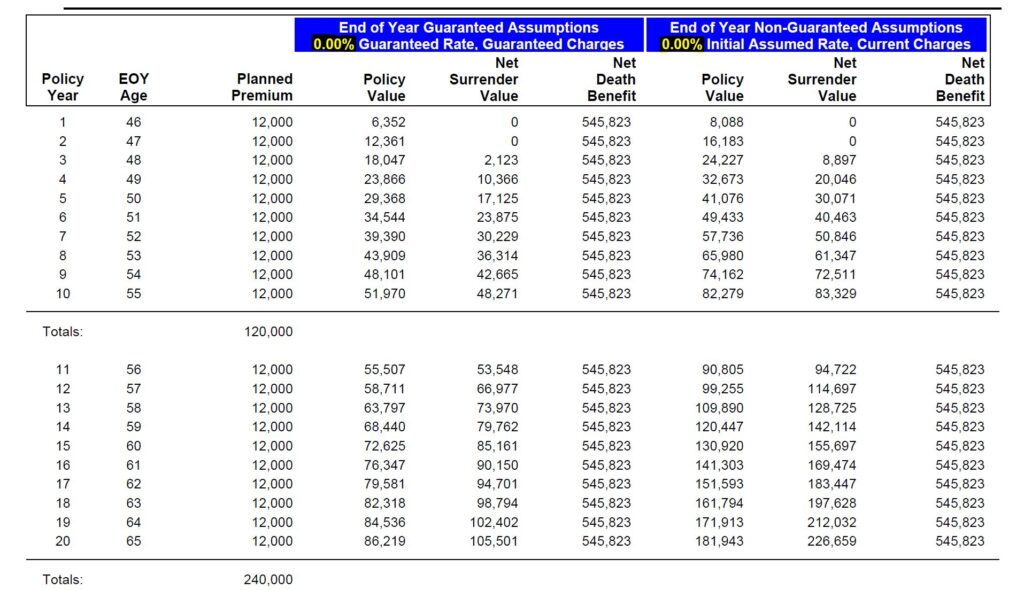

We looked at a hypothetical case for a 45-year-old male (Best Non-Smoker) in Connecticut, funding a policy with $12,000 per year. To test the integrity of the design, we assumed a 0% index credit for the first 20 years consecutively.

In a traditional investment account, 20 years of 0% growth while paying fees would be catastrophic. However, in a properly structured IUL, the story is different:

The Power of the Floor: The 0% floor ensures that while the policy earns no interest in a down year, the cash value is strictly protected from negative index returns.

Intentional Overfunding: Even with 0% crediting, the account value in our model continued to grow. This is because the policy was funded using a minimum non-MEC death benefit and maximum allowable premium.

Premium vs. Charges: Because more of every dollar is directed toward the cash value rather than pure insurance charges, the policy builds momentum that offsets internal costs.

20-year hypothetical IUL illustration.

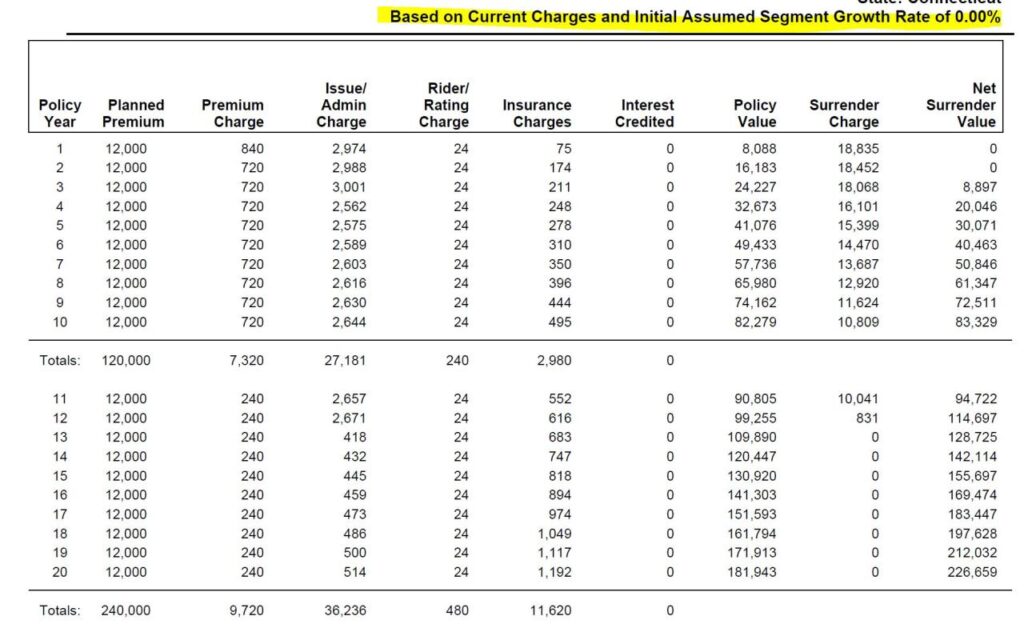

20-year hypothetical IUL illustration breakdown of charges.

The myth of the collapsing IUL usually stems from poor design; policies that are underfunded or carry a death benefit that is too high, causing insurance charges to eat the principal.

In our Zero Can Be Your Hero model, the policy doesn’t just survive; it thrives for decades. In fact, under these extreme 0% assumptions, the policy does not lapse until age 91. When you consider that it is statistically nearly impossible for the market to post 0% or negative returns for 20 consecutive years, the safety margin becomes even more apparent.

For advisors who have been told that IUL is too risky by definition or loses money at zero, this illustration is a necessary second look. It demonstrates that the outcome of an IUL policy is dependent on design and funding strategy as much as market performance.

It is important to remember that, at its core, an IUL is a life insurance contract, and like any permanent structure, there are internal costs associated with the death benefit protection. These mortality and expense charges are the trade-off for the security the policy provides. However, our scenario highlights why design is the ultimate equalizer. By intentionally overfunding the policy—pairing a minimum non-MEC death benefit with the maximum allowable premium—we direct as much capital as possible toward the cash value. This strategy helps ensure that even in flat years, the growth from the premium itself can outpace the pure insurance charges, preventing the policy from stagnating or losing ground.

Do you have a perplexing case requiring expert advanced design? Reach out to us at OnTheCase@ThreePointsInsuranceDesign.com today.